kpss test in r package|how to test for stationarity : service To perform a KPSS (Kwiatkowski-Phillips-Schmidt-Shin) test in R, we can use the urca package. This package provides functions to conduct unit root tests, including the KPSS test. Prepare your time series data. Ensure that . Sejam bem-vindos ao melhor e maior site de Acompanhante.

{plog:ftitle_list}

WEBComprobar Primitiva con QR. Comprueba tus Boletos de Primitiva con la cámara de tu móvil. Escaneando QR. Preparando la cámara.. Apunta la cámara de tu móvil al QR del boleto. Si no le funciona la lectura de QR .

Computes the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test for the null hypothesis that x is level or trend stationary. To perform a KPSS (Kwiatkowski-Phillips-Schmidt-Shin) test in R, we can use the urca package. This package provides functions to conduct unit root tests, including the KPSS test. Prepare your time series data. Ensure that .

The KPSS test in R can be performed using the kpss.test() function from the tseries package. This function calculates the KPSS test statistic and compares it to the critical values .Performs Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test for the null hypothesis that x is a stationary univariate time series. To perform a KPSS test in R, you need to first install the tseries package. Then, you can use the kpss.test() function to run the KPSS test. This function takes in a time series as its argument and returns the test statistic, p .

This function computes the Kwiatkowski-Phillips-Schmidt-Shin test statistic for examining the null hypothesis that a given series is level-stationary, or stationary around a deterministic trend . To perform the KPSS test in R, we can use the “ur.kpss” function from the “urca” package. The function takes as input a time series and returns the test statistic along with its p .

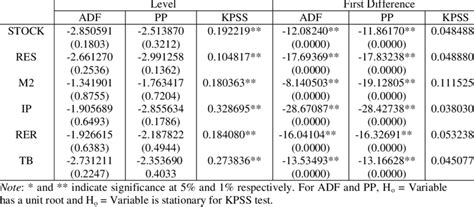

Two statistical tests would be used to check the stationarity of a time series – Augmented Dickey Fuller (“ADF”) test and Kwiatkowski-Phillips-Schmidt-Shin (“KPSS”) test. A method to convert a non-stationary time series into .

The problem with R is that there are several packages that can be used for unit root tests. Just to mention another one, > library (tseries) > adf.test (X,k=0) Augmented Dickey .Performs the Augmented Dickey-Fuller test for the null hypothesis of a unit root of a univarate time series x (equivalently, x is a non-stationary time series). Rdocumentation. powered by. Learn R Programming. aTSA (version 3.1.2.1) Description. Usage Value, , . How to Implement the KPSS Test? In python, the statsmodel package provides a convenient implementation of the KPSS test. A key difference from the ADF test is the null hypothesis of the KPSS test is that the .

Performs stationary test for a univariate time series. Rdocumentation. powered by. Learn R Programming. aTSA (version 3.1.2.1) Description. Usage Value, , Arguments. Author. Details, . . method = "kpss") # same as kpss.test(x) Run the code above in your browser using .

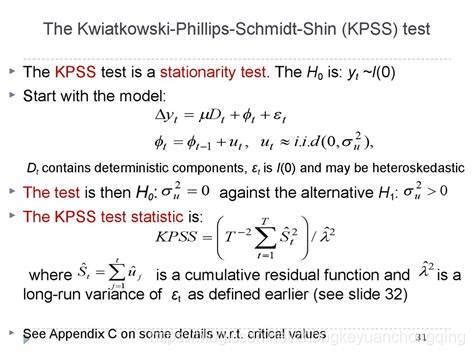

Hence, this test reduces to simply test the hypothesis that \{ \xi_t \} is stationary, that is, H_0: \sigma^2_z = 0. The test statistic combines the one–sided Lagrange multiplier (LM) statistic and the locally best invariant (LBI) test statistic (Nabeya and Tanaka, (1988)). KPSS test; Here, in the KPSS testing procedure, two models can be considerd : with a drift, or with a linear trend. Here, the null hypothesis is that the series is stationnary. . One more time, it is possible to use another package to get the same test (but again, a different output) > kpss.test(X,"Level") KPSS Test for Level Stationarity . Performs the KPSS unit root test, where the Null hypothesis is stationarity. The test types specify as deterministic component either a constant "mu" or a constant with linear trend "tau". . R Package Documentation. rdrr.io home R language documentation Run R code online. Browse R Packages.x <- rnorm(1000) # is level stationary kpss.test(x) y <- cumsum(x) # has unit root kpss.test(y) x <- 0.3*(1:1000)+rnorm(1000) # is trend stationary kpss.test(x, null = "Trend") [Package tseries version 0.10-56 Index ]

jarque.bera.test: Jarque-Bera Test; kpss.test: KPSS Test for Stationarity; maxdrawdown: Maximum Drawdown or Maximum Loss; na.remove: NA Handling Routines for Time Series; NelPlo: Nelson-Plosser Macroeconomic Time Series; nino: Sea Surface Temperature (SST) Nino 3 and Nino 3.4 Indices; plotOHLC: Plot Open-High-Low-Close Bar Chart

KPSS test is a statistical test to check for stationarity of a series around a deterministic trend. Like ADF test, the KPSS test is also commonly used to analyse the stationarity of a series. However, it has couple of key differences compared to the ADF test in function and in practical usage. Therefore, is not safe to just use them interchangeably. We'll . jarque.bera.test: Jarque-Bera Test; kpss.test: KPSS Test for Stationarity; maxdrawdown: Maximum Drawdown or Maximum Loss; na.remove: NA Handling Routines for Time Series; NelPlo: Nelson-Plosser Macroeconomic Time Series; nino: Sea Surface Temperature (SST) Nino 3 and Nino 3.4 Indices; plotOHLC: Plot Open-High-Low-Close Bar Chart I've been trying to create an ARIMA model however, I'm not sure how to determine if the data is stationary or not. I preformed a KPSS test in R using kpss.test from package tseries and these are the results:. KPSS Level = 1.966, Truncation lag parameter = 5, p-value = 0.01 Warning message: In kpss.test(coke[,5], null = "Level") : p-value smaller than printed p .

I'm using R to calculate the KPSS to check the stationarity. The library that I'm using is tseries and the function is kpss.test I have done a simple test using cars (a default matrix on R). The.

A KPSS test can be used to determine if a time series is trend stationary.. This test uses the following null and alternative hypothesis: H 0: The time series is trend stationary.; H A: The time series is not trend stationary.; If the p-value of the test is less than some significance level (e.g. α = .05) then we reject the null hypothesis and conclude that the time series is not .

The KPSS (Kwiatkowski-Phillips-Schmidt-Shin) test was conducted on the lh dataset, resulting in a KPSS Level statistic of 0.29382 with a truncation lag parameter of 3. The associated p-value is 0.1. In the context of the test for level stationarity, a p-value greater than the significance level (commonly 0.05) suggests that we fail to reject .See adf.test for more details. type: the test type, only valid for method = "pp". See pp.test for more details. lag.short: a logical value, only valid for method = "pp" or "kpss". See pp.test and kpss.test for more details. output: a logical value indicating to print the results in R console. The default is TRUE. I am using the KPSS test from the R urca package.. My result is the following: $resProp.Dwell.3 ##### # KPSS Unit Root Test # ##### Test is of type: tau with 3 lags.

Kwiatkowski-Phillips-Schmidt-Shin test for stationarity. Computes the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test for the null hypothesis that x is level or trend stationary. Parameters: ¶ x array_like, 1d. The data series to test. regression str {“c”, .KPSS test: don`t reject H0. Both imply that series is stationary. Case 3 If we can’t reject both test: data give not enough observations. Case 4 Reject unit root, reject stationarity: both hypothesis are component hypothesis – heteroskedasticity in series may make a big difference; if there is structural break it will affect inference.1.R语言函数ur.kpss() 对于一个时间序列,例如用R自带的google股价变化数据goog(可以通过导入fpp2包之后直接使用goog这个数组变量,这里仅为示例,代指要检验的时间序列或者数组)。 . (1)比较显然地,检验的结果是用 Value of test-statistic:10.7223,来和下面最下面的4 .

Functions to estimate the number of differences required to make a given time series stationary. ndiffs estimates the number of first differences necessary.Performs the Phillips-Perron test for the null hypothesis of a unit root of a univariate time series x (equivalently, x is a non-stationary time series). Rdocumentation. powered by. Learn R Programming. aTSA (version 3.1.2.1) Description. Usage Value,, , , Arguments.. Author. Details . KPSS Test in R, the KPSS test (Kwiatkowski-Phillips-Schmidt-Shin) is a statistical test used to determine whether a time series has a unit root or not. . To perform the KPSS test in R, we can use the “ur.kpss” function from the “urca” package. The function takes as input a time series and returns the test statistic along with its p .

kwiatkowski phillips schmidt shin test

We would like to show you a description here but the site won’t allow us.

In VGAMextra: Additions and Extensions of the 'VGAM' Package. View source: R/KPSS.test.R. KPSS.test: R Documentation: KPSS tests for stationarity Description. The Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test for the null hypothesis that the series x is level or trend stationary UsageDetails. To estimate sigma^2 the Newey-West estimator is used. If lshort is TRUE, then the truncation lag parameter is set to trunc(3*sqrt(n)/13), otherwise trunc(10*sqrt(n)/14) is used. The p-values are interpolated from Table 1 of Kwiatkowski et al. (1992). If the computed statistic is outside the table of critical values, then a warning message is generated.This is an interface to the unitroot tests implemented by B. Pfaff available through the R package urca which is required here. Added functions based on the urca package include: urdfTest: Augmented Dickey-Fuller test for unit roots, . KPSS Test for Unit Roots: Performs the KPSS unit root test, where the Null hypothesis is stationarity. .

This post explains how to use the augmented Dickey-Fuller (ADF) test in R. The ADF Test is a common statistical test to determine whether a given time series is stationary or not. We explain the interpretation of ADF test results from R package by making the meaning of the alphanumeric name of test statistics clear. ADF test

custom moisture meter for sheetrock

custom moisture plant meter

webGoogle Search Console. Improve your performance on Google Search. Search Console tools and reports help you measure your site's Search traffic and performance, fix .

kpss test in r package|how to test for stationarity